Fintech’s US Charter Rush 2025-26: The New Race for Deposits and Rails

The fintech race to own funding, rails, and regulation

Welcome to Fintersections, where we explore how fintech models evolve as they collide with broader shifts in banking, and consumer behaviour. In this edition, we explore why fintechs are racing for US bank charters as partner-bank models become costlier and more fragile. The blog maps how digital banks, BNPL players, payment processors, and crypto firms are using licences to own funding, rails, custody, and regulatory control.

For more than a decade, fintech’s thesis was simple: build what banks wouldn’t - instant credit at checkout, mobile-first money management, frictionless payments, without carrying the weight of being a regulated institution. They thrived by renting bank infrastructure (deposits, charters, compliance) while owning the customer touchpoints. And that served them well, until it didn’t.

What changed is that “rent-a-bank” stopped feeling like a shortcut and started feeling like a ceiling. As fintechs scaled, the partner model increasingly meant:

higher structural funding costs vs. insured deposits,

shared economics on the most valuable layers (deposits, lending margin, network

access), and operational fragility when a sponsor bank’s risk appetite, or a regulator’s interpretation, shifted.

For countries like the US, these pressures are amplified by a bank-first system that’s also more concentrated. The number of US banks fell from 8,500 (2008) to ~4,500 (2025). This raises the stakes around who gets to enter the system and on what terms. Trust still tilts toward incumbents: 68% of the general population trust banks vs. 53% for fintechs (and 43% for crypto/digital assets). And so do unit economics: chartered fintechs average 14–16% ROE vs. 9–10% for non-banks, largely because insured deposits are cheaper than wholesale or partner-bank funding (often adding ~1.5–3% to the cost of money).

This is where the fintech identity narrative flipped in 2025. After years of ecosystem building via BaaS partnerships, both domestic and international players are aggressively pursuing US bank charters for bank-like regulatory privileges. Just the first eight months of 2025 produced 21 applications, over twice the total of 8 from entire 2024. In a market that remains the global deal epicenter (44% of global fintech deals; ~2,112 deals in 2025), the incentive to “own the perimeter” has rarely been stronger.

Under this context, we now map the fintech business models driving this charter rush, and decode the different charter paths they’re choosing to secure a durable edge in the US market.

See further in Fintech with WhiteSight Radar. 🔮

Unlock a treasure trove of fintech intel with a WhiteSight Radar subscription. See further with exclusive reports, industry trend breakdowns, and expert analysis on everything from Embedded Finance and Digital Banking to Open Finance and beyond.

Become a member and steer your business course with actionable intelligence on the winning strategies of leading companies like Klarna, Nubank, Revolut, SoFi, Adyen, Stripe, Starling Bank, Affirm, and Toast that propels your business to the forefront of fintech. (PLUS! More in our premium content pipeline - Amazon, Grab, Wise, Shopify, Mercado Libre… the list goes on!)

Supercharge your Fintech IQ with WhiteSight Radar, putting expert fintech intel at your fingertips! 🧭

A Brief History of US Charters (1999 → 2026)

To understand why 2025–26 feels like a charter renaissance, start with a US-specific reality:

US banking is a license-driven market. The Office of the Comptroller of the Currency (OCC) charters national banks, the Federal Deposit Insurance Corporation (FDIC) approves deposit insurance, the Federal Reserve governs the monetary system access and holding-company oversight, and state regulators oversee state charters. A bank charter offers nationwide operating, FDIC-insured deposit-taking (with approval), and direct connectivity to Fed payments systems. That’s why the charter interest comes in waves, where value of ownership rises and falls with regulation, rates, and risk appetite.

1999: Charters were common because banking was profitable and expanding: In 1999, the US launched 270 new banks in a single year, three times the total formed across 2010–2025 combined. This boom was fueled by two decades of higher interest rates

and deregulation. A key inflection point was the Depository Institutions Deregulation and Monetary Control Act (1980). It lifted deposit-rate caps, expanded who could offer bank-like accounts, and standardized Fed control. This allowed banks to compete aggressively on price, products, and geography.

2008–early 2010s: Post-crisis reform made “starting a bank” structurally harder: After the financial crisis, the incentives flipped. Dodd-Frank (2010) brought tighter supervision and systemic-risk guardrails, most visibly through tougher stress testing and capital planning. Meanwhile, the global Basel III framework raised the quality and quantity of capital and added liquidity standards. The message was clear: banking is now a high-fixed-cost, high-scrutiny business.

2010s: The fintech workaround to build around banks, not as banks: US licensing is fragmented: federal charters typically run through the OCC, while states charter their own banks (with federal overlay). Non-bank models (payments, wallets, remittance) often needed 50+ state money transmitter licenses to operate nationally. This is why fintechs partnered with smaller regional banks, which provided them with FDIC-insured deposit accounts, lending, and compliance infrastructure. Full bank ownership would drag them into FDIC insurance processes and (often) the Bank Holding Company Act (BHCA), which makes the Fed the umbrella supervisor of any company that controls a bank and limits what non-financial parents can do.

2016–2021: the OCC tries a “fintech charter” on-ramp; litigation turns it into a dead end: In 2016, the OCC floated a special purpose national bank charter tailored for fintechs. It drew interest because it could arguably reduce state-by-state licensing friction. And because it would also not take deposits/FDIC insurance, it could potentially avoid triggering BHCA issues for controlling owners. However, the NY Department of Financial Services (NYDFS) and the Conference of State Bank Supervisors (CSBS) sued because the move threatened state oversight and revenue (state licensing), and because it raised the question: can a federal “bank” charter exist for a firm that doesn’t take deposits the traditional way, and should that charter preempt state consumer/financial rules? Years of litigation turned the idea into uncertainty, and uncertainty killed application pipelines. By early 2021, the fintech charter was effectively dead.

2022-2026: Sponsor-bank fragility meets a changing regime, charters return as strategy: A limited-purpose national trust bank structure emerged as the most practical “federal perimeter” option because it doesn’t take deposits, echoing some benefits of the earlier fintech charter without turning the firm into a full depository bank. But the massive crypto winter in 2022 and consumer losses froze any appetite the already-cautious OCC had for banking experiments.

Then the calculus changed fast, where three catalysts converged:

The sponsor/BaaS model started looking like counterparty risk: Fintechs learned that when you rent the perimeter, you inherit your partner’s risk tolerance, and their regulator’s. The Synapse collapse (touching banks like Evolve Bank & Trust) exposed how messy “who owns the ledger” becomes when middleware breaks: access freezes, reconciliation disputes, and public scrutiny. Regulators began issuing joint guidance on risks in bank–third-party deposit arrangements, reflecting heightened scrutiny of bank-fintech models.

Higher rates made deposits strategically valuable again: Fintechs began earning a significant portion of revenue from interest income, even if their core proposition wasn’t exactly focused on digital banking. One signal of this was payments-led Revolut reporting over 25% share of revenue from interest income in 2024.

Regulators became more open, especially to bringing crypto/fintech inside the perimeter: Under the Trump administration, regulators have signaled a lighter, more open posture, creating a timely window for charter bids. The OCC’s Office of Innovation built engagement muscle by encouraging early, frequent dialogue, while the FDIC signaled more openness to innovative deposit insurance applications. Congress’ GENIUS Act (2025) created a federal framework for payment stablecoins, including pathways for regulated issuers and OCC oversight for certain federally licensed non-bank issuers. As of 2025, US incumbents are already using blockchain to compress settlement delays, reclaim custody, and keep tokenized flows inside the traditional financial system. More on how this shift in our infographic “Banks, Blockchains, and the American Blueprint”

The result is a more “strategy-based” charter era, where each is chosen based on which bank privileges a fintech can no longer afford to outsource. The deeper shift is that fintech is maturing towards governance, where licenses, funding, and regulatory posture are becoming competitive weapons. We unpack this evolution in “Fintech’s Journey: From Hustlers to License Holder”.

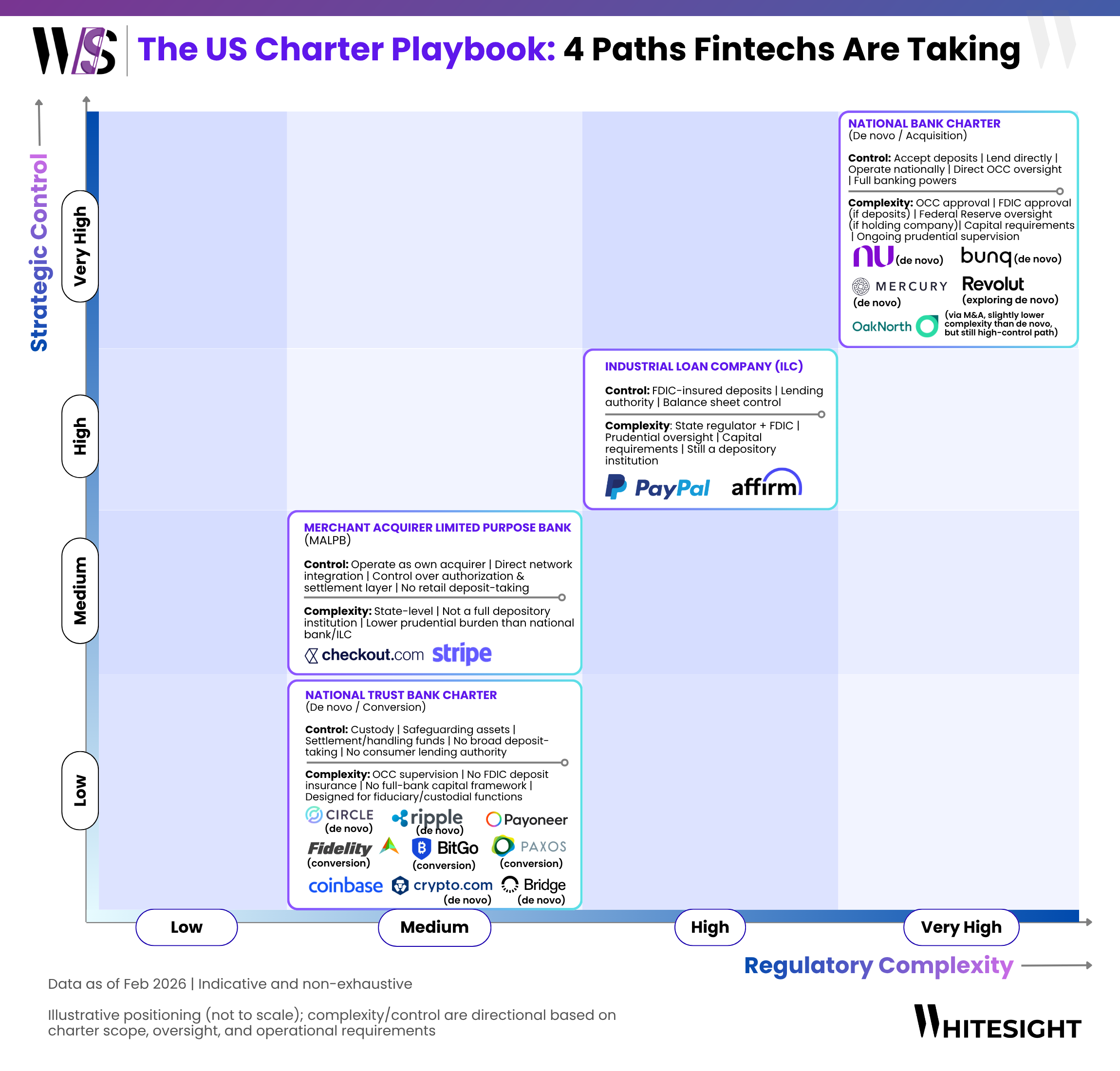

The Four Paths Unlocking Different Parts of Banking

Fintechs are choosing four distinct charter paths based on what part of the financial stack they most want to own: funding, lending, network access, or trust.

BNPL worked because it solved three pressures at once. Merchants subsidize the model via discount fees that increase conversion and basket sizes. Consumers face a lower barrier to credit than traditional revolving cards. And for providers, the app became a repeat-engagement ecosystem that kept users coming back to browse, buy, and borrow again.

National Bank Charter: the full-stack move for digital banks

National trust bank charters allow companies to offer custodial services, including safeguarding customer funds and handling settlements under a single regulator (the OCC). Both consumer and business digital banks like Nubank, bunq, Mercury, Revolut, and OakNorth (via acquisition) go for these charters because their product promise is inseparable from balance-sheet ownership. They are trying to become multi-product ecosystems where deposits are the engine, lending is the monetization layer, and payments are the daily habit. At scale, sponsor-bank reliance becomes a hard constraint: it can limit onboarding, pricing, product expansion, and continuity. So, these players bring the license layer in-house, turning compliance into a moat.

Industrial Loan Company (ILC): the lender’s funding upgrade

ILCs are a step down in complexity: FDIC-insured and lending-capable, yet typically without full bank-holding-company treatment. That makes them ideal for specialist lenders like PayPal and Affirm, whose core constraint is funding cost and margin retention. For theselenders, the difference between traditional bank funding (~2–3%) vs non-bank funding (~5.5–7%) is considerable, where this delta makes the difference between good unit economics and structurally losing to chartered competitors. Block (then Square) is the blueprint. It first applied for the charter in 2017, won FDIC conditional approval in 2020, and launched Square Financial Services in 2021. It first used the charter to originate business loans and build deposit products, then steadily pulled more lending economics in-house. And even non-banks have joined the ILC wave. Nissan Motor Acceptance Corp. filed to form an ILC in 2025 (under review), and in Jan 2026 the FDIC approved deposit insurance for Ford Credit Bank and General Motors Financial Bank (Utah ILCs). These firms are essentially trying to fund and expand auto + dealer financing nationwide with better efficiency and pricing, strengthening dealer ties in the process.

Merchant Acquirer Limited Purpose Bank (MALPB): payments firms going directly into the network layer

A MALPB charter is a Georgia-specific, limited-purpose banking designation allowing payment processors to directly access credit card networks (e.g., Visa, Mastercard) without relying on third-party sponsor banks. Checkout.com’s route is targeted: an ILC or national bank would be overkill for a processor that mainly wants to remove the “sponsor bank tax” in acquiring. Stripe’s 2025 MALPB approval fits the same playbook: it’s designed to unlock direct Visa/Mastercard membership in the US and process payments without a BIN sponsor. For processors like Stripe and Checkout, becoming a network node means tighter control of authorization/settlement mechanics, lower per-transaction dependency, and improved margin structure, and that’s exactly what the MALPB charter enables.

National Trust Bank: crypto’s bid for regulated custody

Trust charters are built for fiduciary and custodial functions: safeguarding assets, handling settlement, and acting as a regulated trust entity, without broad deposit-taking or consumer lending authority. They sit under OCC supervision and typically don’t involve FDIC insurance. Stablecoin issuers and crypto exchanges cluster here because it fulfills their immediate need to make custody and settlement “institution-grade,” bring key functions inside a recognized supervisory perimeter, and (where relevant) connect more directly to core payment rails (Fedwire, ACH, and potentially FedNow).

It’s clear that different licenses unlock different advantages. But the next question is which certain business models are showing up in the charter queue right now, and why.

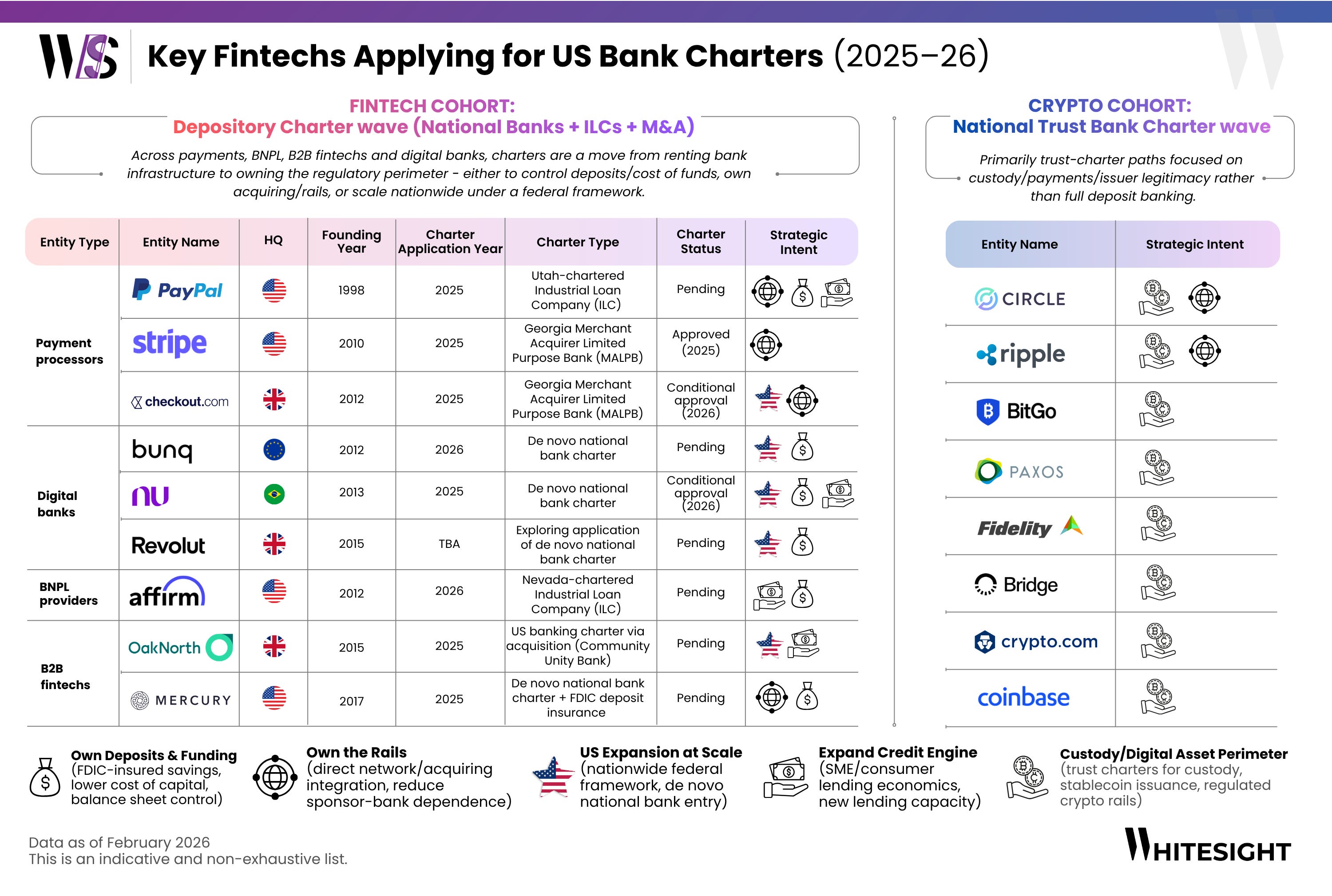

The Five Business Models Chasing the US Charter Moment

The 2025–26 filers are fintechs that have already solved distribution (brand + embedded channels) and carry meaningful volume (payments, deposits, lending). Across digital banks, BNPL, B2B neobanks, payment processors (and a smaller crypto cohort), the shift is from renting bank infrastructure to direct regulatory standing: cheaper funding, tighter rail control, and nationwide scale under a clearer regulatory framework.

The interesting part is why these specific models are applying now, and what their trail of previous moves says about where fintech economics are headed:

1. Digital banks: Foreign digital banks have long struggled to establish a US banking foothold because de novo (new) charters demand time, capital, and regulatory stamina. Nubank is notable for breaking that pattern on speed: it received conditional OCC approval on Jan 29, 2026, after filing on Sep 30, 2025 (a 121-day turnaround), suggesting a more navigable path for scaled, well-prepared applicants. It arrived profitable and massive: 127M customers, $4.2B quarterly revenue, 31% ROE, $783M net income (Q3 2025), and an estimated $0.90/month cost-to-serve vs. $5+ for traditional banks. What Nubank is really exporting to the US is a proven operating machine where profitability comes from radically low servicing costs at massive scale. Uncover a deeper breakdown of Nu’s model in detail in our Nubank Deep Dive Report. Revolut is the next “global digital bank” candidate aiming for similar footing, arguing the US is credit-driven and meaningful expansion requires a license. It is echoing the LendingClub/SoFi playbook: enter via an existing regulated entity/regulated permissions than “partner-bank” the way into full credit economics. Revolut’s long-term ambition has always been broader than payments: credit cards, lending, and wealth are where the revenue unlock sits, and the US is the hardest market to do that without a license. Get more details on this expansion logic in our blog “Revolut’s G7 Playbook: Building Global Financial Influence”. Meanwhile, bunq represents the “second attempt”, after withdrawing a prior OCC bid following a 301-day wait. With the timing and the regulator’s stance different now, it’s reapplying with a wedge around globally mobile customers, starting in expat-heavy metros and using European records to help newcomers build US credit history.

-Category move: For digital banks, the endgame is vertical integration: stop negotiating the roadmap with sponsor banks, fund with insured deposits, and capture the full spread when they turn deposits into credit.

2. BNPL providers: Affirm’s ILC bid fits BNPL’s evolution into a scale lending business where cost of funds drives pricing and merchant adoption. It’s applying via Nevada + FDIC to gain capital flexibility and the stability of an insured funding base. Moreover, a national bank/charter path can drive a materially lower cost of capital. Its FQ3’25 shareholder letter put average funding costs at ~7.1%, while chartered peers like SoFi fund at ~4–5%, a gap worth roughly $551.9M in annualized savings from a cheaper funding mix. Timing is also at play, as regulators have recently provided ILC approvals to Ford and GM, reinforcing that the ILC lane is active and limited.

-Category move: BNPL’s next phase is moving towards credit infrastructure. As regulators reopen the ILC lane, the category is splitting into two: those who can fund cheaply and those who will permanently pay a higher rent for capital.

3. B2B neobanks: Mercury’s OCC charter + FDIC bid follows a live stress test: during the SVB collapse, it reportedly attracted $2B in deposits in five days. As an account-led platform with 3 years of GAAP profitability, ~$650M annualized revenue, and 200K+ customers, partner-bank dependency becomes a structural bottleneck the moment the partner can’t scale (or can’t onboard). A charter turns that dependency into control: onboarding, product pace, and lending directly against deposits. Separately, OakNorth is taking the acquisition route, buying Community Unity Bank after Fed/NYDFS approval for a NY representative office in 2024. This shows how it established presence, proved demand, and then got the charter to scale lending nationwide.

-Category move: The category move is from “banking interface” to banking control. When the core product is the account, charter logic is about controlling onboarding, continuity, pricing, and eventually lending against deposits - without sponsor dependency.

4. Payment processors: PayPal’s Utah ILC bid (“PayPal Bank”) matches its hybrid model: payments distribution plus SME credit. Since 2013, it has provided access to $30B+ in loans/working capital to 420K+ business accounts, but US originations still run through WebBank, a classic bank-by-partnership. An ILC would reduce that dependency, widen funding options (including insured deposits), and tighten the loop between deposits, risk, and product design. Checkout.com is more “rails-native.” Its Georgia MALPB approval supports in-house acquiring and deeper network integration with card networks upon full approval, cutting intermediaries and US acquiring friction. It also fits Checkout’s recent trajectory: US is the fastest growing revenue contributor for the company, with volumes growing at ~70% in 2025 as more enterprises choose Checkout.com.

-Category move: It signals a land grab for network adjacency: processors want to become nodes in the card ecosystem. They now want to own settlement and attach credit where the margin pool is deeper.

5. Crypto firms: Many crypto firms are favoring national trust bank charters for custody and settlement legitimacy, not deposit banking. For stablecoin issuers and digital-asset players, this solves credible redemption, safeguarding, and operational resilience when markets stress, backed by clearer governance and OCC oversight.

The Next Era of Fintech is License-led

The charter wave is still more “in motion” than “done”, where several headline filings remain pending (PayPal, Mercury, bunq, Coinbase, Crypto.com). There’s also a growing pipeline of the “next cohort” testing the window: Monzo is weighing a fresh bid, Starling has explored buying a US bank to accelerate entry, and Airwallex also is exploring a US bank acquisition. As for industry-wide expectations, BaaS is likely to persist for asset-light and early-stage fintechs, but with higher scrutiny and tighter economics. Incumbents will also feel the squeeze slowly, with better rates and tighter product bundles being offered from chartered fintechs, even if branches still defend deposits in the near term. As for consumers and SMBs, they will benefit most where charters remove friction: faster onboarding, sharper pricing, and fewer partner-bank edge

For BNPL firms, expenses generally fall into the following buckets: funding costs, processing and servicing, technology and data infrastructure, and sales and marketing. Affirm and Klarna share these same cost centers, but the way those costs scale, and the way technology and partnerships reshape them, tells a deeper story about their operating models.

And It’s A Wrap! 👏

Hope you enjoyed this edition of Fintersections! Stay tuned for more interesting think-pieces in the coming months.

Hungry for more fintech insights? Check out some of our other work at WhiteSight.

Our latest publications include:

If you're someone who likes to stay in the know of what’s happening in FinTech, you don’t want to miss out on our bi-weekly newsletter -Future of Fintech - where we religiously track next-gen themes of the industry.

We also track Onchain Finance and Agentic AI updates.

Fintech research is in the WhiteSight DNA, so if you'd like to get in touch for features, research content, or sponsorship-related services, reach out to us at hello@whitesight.net.

And lastly, to stay updated on everything fintech, follow us on LinkedIn and Twitter and don't be shy to show some 💛

Future revenues will not derive from what you own, but what you enable, command, and responsibly grow.

The danger is not FinTechs. It is irrelevance. The reward is not market share, it is trust-share.

The US Charter Rush is definitely something to keep up with!