Affirm vs Klarna: One BNPL Story, Two Very Different Endgames

Where does pay-later go next?

Welcome to Fintersections, where we explore how fintech models evolve as they collide with broader shifts in banking, and consumer behaviour. In this edition, we look at how the next chapter of BNPL is being shaped by two of its biggest names: Affirm and Klarna. While both emerged from the same checkout-financing wave, they are now scaling in very different directions. One toward payments, the other toward digital banking.

For decades, consumer credit largely meant one thing: the credit card. A revolving line of credit, high interest ticking in the background, and the constant balancing act between convenience and debt. Then, Buy Now, Pay Later (BNPL) emerged as a cleaner alternative to solve this tension. It reframed credit as a structured, short-term commitment tied to a specific purchase with little-to-no interest rates.

See further in Fintech with WhiteSight Radar. 🔮

Unlock a treasure trove of fintech intel with a WhiteSight Radar subscription. See further with exclusive reports, industry trend breakdowns, and expert analysis on everything from Embedded Finance and Digital Banking to Open Finance and beyond.

Become a member and steer your business course with actionable intelligence on the winning strategies of leading companies like Apple, Nubank, Revolut, SoFi, Adyen, Stripe, Starling Bank, OakNorth Bank, and Toast that propels your business to the forefront of fintech. (PLUS! More in our premium content pipeline - Amazon, Grab, Wise, Shopify, Mercado Libre… the list goes on!)

Supercharge your Fintech IQ with WhiteSight Radar, putting expert fintech intel at your fingertips! 🧭

The idea was not entirely new

It echoed layaway programs from the 1930s, which let shoppers pay over time before taking an item home, until credit cards displaced them in the 1980s. Early digital installment products like PayPal Credit in the 2000s later carried that logic online. What modern BNPL changed was speed and context. Approval moved to checkout. Repayments became instant, app-led, and mobile-native. Credit started behaving like part of the payment flow itself. Before the pandemic, BNPL was still a small corner of consumer finance. Then ecommerce surged, online checkout became the storefront, and installment options moved from niche to norm.

The appeal is obvious.

→ For consumers, BNPL lowers the psychological barrier to purchase, making spending feel smaller and easier to budget - particularly for younger consumers wary of revolving credit card debt. For merchants, it can lift average order values by 20–40% while improving checkout conversion rates.

What began with fashion and electronics now spans travel, groceries, and everyday spend. In the 2025 holiday season alone, Americans spent more than $20B via BNPL services, highlighting how deeply installment-based payments have embedded themselves into everyday commerce. And the industry’s momentum shows no signs of slowing, with user adoption projected to surpass 900 million globally by 2027, up from 360 million in 2022 (up 157%).

However, before cards, wallets, and banking layers entered the picture, the first flywheel was online retail: more checkout integrations, more merchant adoption, and more digital-native shoppers getting comfortable with installment payments. We’ve mapped this earlier partnership wave in our report, “2023 Roundup: The Synergy of BNPL and E-commerce”, which tracks how ecommerce-BNPL collaborations helped push the model from niche to norm.

This rise, however, has brought sharper scrutiny:

In the US, the CFPB withdrew its 2024 interpretive rule in 2025, stating that it doesn’t believe that BNPL lending is appropriate for credit card regulations. As of now, enforcement action is predominately at the state level.

In Europe, the revised Consumer Credit Directive (CCD II) broadens consumer-credit rules and must be applied from November 2026.

In the UK, BNPL will come under FCA regulation from July 15, 2026. HM Treasury’s legislation aims to boost consumer protection, transparency, and to promote responsible lending.

Australia has already brought BNPL under stronger credit regulation via the The Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024 (Cth). It regulates BNPL products as credit products, and took full effect in June 2025, requiring providers to obtain credit licences.

Around the world, BNPL is increasingly treated as credit infrastructure. Regulators are looking at installment products as a form of credit that can spill into broader financial services. That shift matters because licensing increasingly determines how far a BNPL player can move into cards, wallets, deposits, and other banking-like layers. We explored this dynamic in our work on “The License Ladder: BNPL Licensing Spectrum in Mexico”, which maps how different regulatory permissions can shape the range of products BNPL firms are able to build.

As BNPL spreads across payments, wallets, and banking services, the boundaries between installment lending, digital banking, and payment networks are beginning to blur. BNPL is fast becoming a strategic wedge into the broader financial ecosystem.

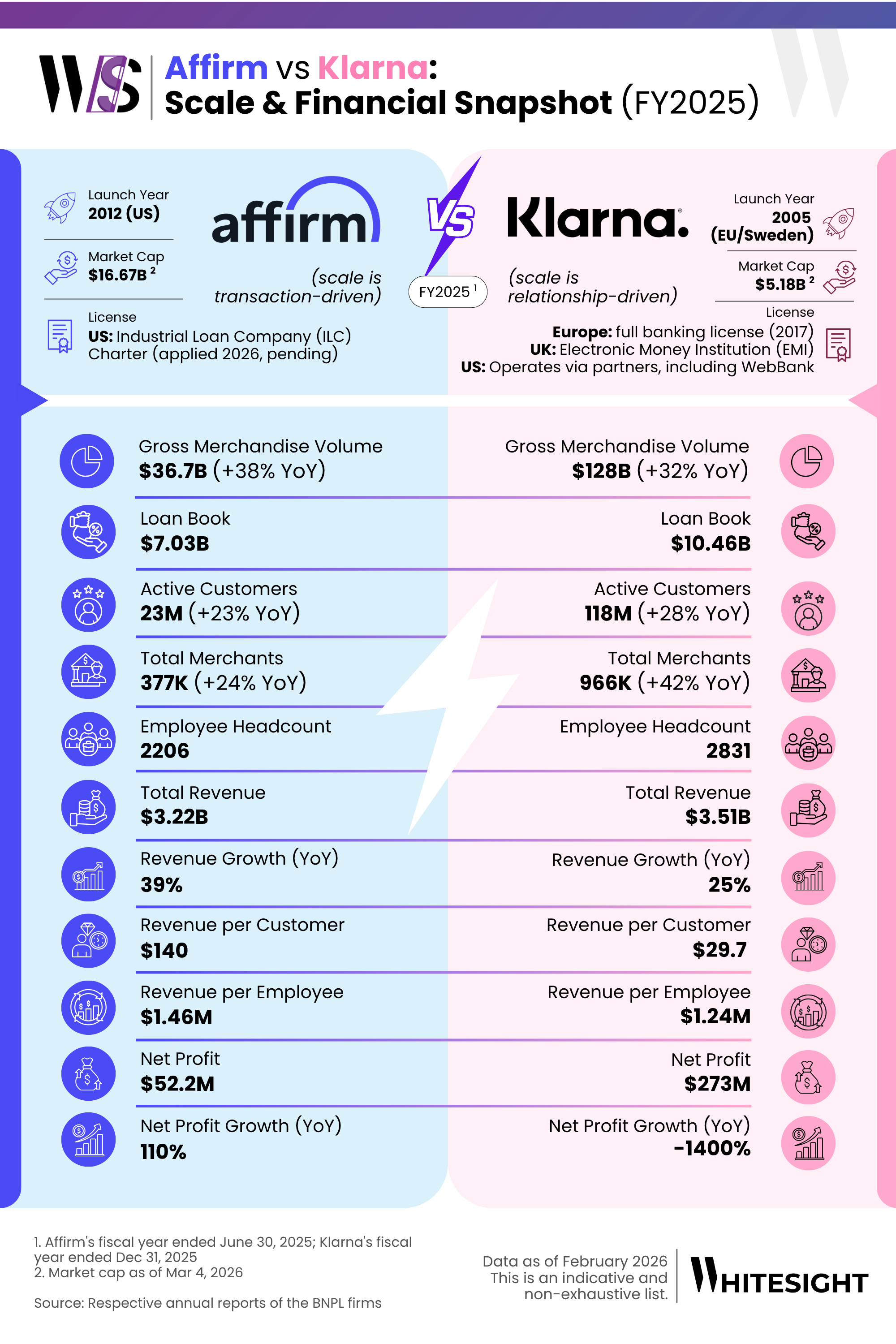

Few companies illustrate this transformation better than Affirm and Klarna. Born from the same BNPL wave, the two firms now appear to be evolving toward very different futures: the former increasingly shaping a new payments network; the latter edging closer to becoming a digital banking platform.

From BNPL Origins to Two Different Scale Models

BNPL worked because it solved three pressures at once. Merchants subsidize the model via discount fees that increase conversion and basket sizes. Consumers face a lower barrier to credit than traditional revolving cards. And for providers, the app became a repeat-engagement ecosystem that kept users coming back to browse, buy, and borrow again.

Klarna and Affirm emerged from this same structural shift:

Klarna, founded in Stockholm in 2005, initially focused on making online checkout easier for merchants and shoppers. Over time, it expanded its merchant footprint across Europe, notably through the acquisition of SOFORT (2014), enhancing its account-to-account payment capabilities. Its trajectory changed more fundamentally in 2017 when it secured a Swedish banking license. That license allowed Klarna to introduce deposits, savings products, and debit cards, turning what began as a checkout solution into a broader consumer financial platform.

Affirm, founded in 2012, approached the problem from a different angle. Its early mission focused on transparent credit and creating a more honest lending experience. Fixed-payment loans, no hidden revolving debt, and underwriting tied to individual purchases gave it a cleaner consumer proposition. But it was the later launch of the Affirm Card in 2023 that pushed this model beyond merchant checkout and into everyday spending. Meanwhile, partnerships across merchant, platform, and issuer ecosystems pushed Affirm closer to payments infrastructure. These steps reinforced comparisons to American Express: a lender operating alongside a payments network rather than simply a credit product embedded in a retailer. Today, its expanding embedded partnerships and card strategy reinforce that shift.

What makes the comparison compelling is how scale is shaped differently.

Affirm’s financial profile suggests a business optimized around high-value transaction capture. It does not need to win every consumer relationship if it can earn more each time it shows up at the point of payment. That is the logic of a network business in the making: be present in the right payment moments, underwrite them well, and monetize the flow more deeply via merchant fees, servicing, and card-linked usage.

Klarna’s profile points towards a much broader consumer and merchant reach, lower revenue intensity per customer, and deposit base. It suggests a company prioritizing financial adjacency and relationship breadth over extracting maximum economics from each transaction.

That distinction hints at two very different endgames. Affirm looks like a lender evolving into a payments company, using credit to enter more commerce flows across checkout, cards, issuer partnerships, and embedded lending. Klarna looks more like a consumer finance platform, using BNPL to acquire users and then deepen the relationship through deposits, debit, wallet features, and everyday app engagement.

One wants to be economically denser at the moment of purchase. The other wants to be harder to leave once the purchase is over.

Similar BNPL DNA, Different Revenue Engines

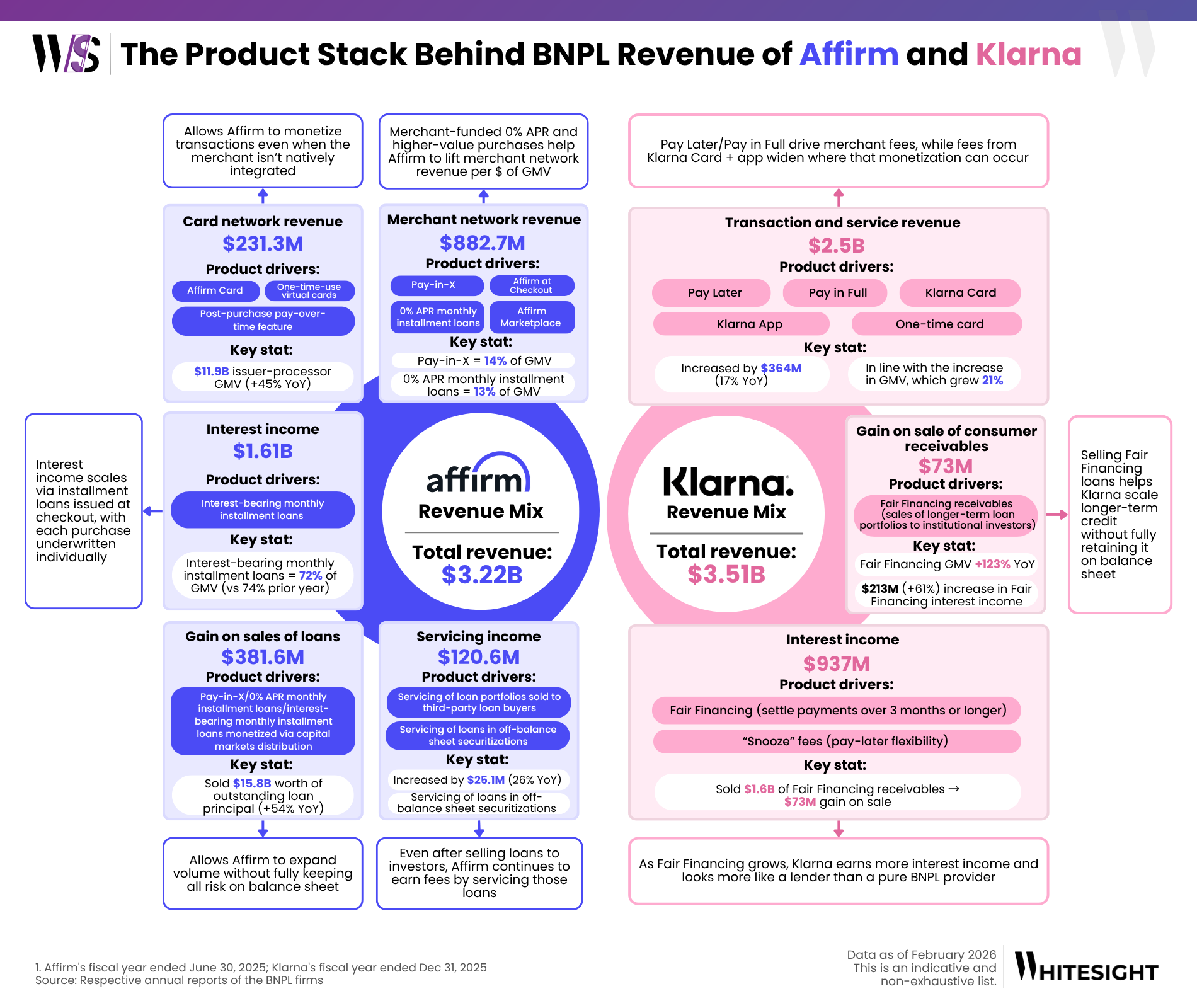

BNPL may have been the entry point, but it was never meant to be the entire business. Once checkout financing proved it could drive conversion and user acquisition, both companies faced the same strategic question: what should come next once the consumer is inside the ecosystem? Their answers have been very different, and those now define how each firm generates revenue:

Affirm expanded beyond installment lending in a deliberate sequence. It began with core checkout products: Pay-in-X (split a purchase into 1-4 interest-free installments), 0% APR promotional loans (consumer pays no interest because merchant subsidizes financing to lift conversion), and interest-bearing installment plans (repaid over longer terms at fixed rates). Together, these products generate two core revenue streams: merchant fees for driving sales and interest income from consumer financing.

Then, it introduced one-time virtual cards so consumers could use Affirm even where merchants were not directly integrated into its network. The Affirm Card debit card (2023) extended that concept further by combining debit-like pay-now functionality with in-app pay-over-time options. This means Affirm now captures revenue from interchange-linked card activity every time consumers route everyday purchases through the card, while also increasing frequency, data, and off-network reach.

From there, loan sales and servicing income added a third layer, where Affirm originates loans and then distributes or services them for third-party capital providers. This makes the business look like a firm building multiple monetization points around the same payment event. This is also why Affirm’s expansion should be read as a distribution story. Virtual cards, card-linked lending, and issuer-led embeds all point to the same goal: placing Affirm in more payment moments without waiting for every merchant to integrate directly.

We unpack this distribution logic in more detail in our blog, “How Affirm is Scaling Distribution with Embedded BNPL”, where we explore how embedded BNPL is moving beyond checkout into consumer and SaaS platforms.

Klarna’s mix is broader and more revealing. Its largest revenue pool still sits in transaction and service revenue, driven by Pay Later, Pay in Full, Klarna Card activity, and app-based merchant monetization. Add to this the longer-term Fair Financing installment product, designed for bigger-ticket purchases and recognized through interest income. But Klarna has also steadily built the app into a commerce discovery platform with search, price comparison, wish lists, and storefronts. This creates advertising revenue through sponsored placements, affiliate marketing, and brand visibility. In 2025 alone, Klarna reported $190M in advertising revenue, which is a strong signal that commerce discovery is now part of the business model.

At the same time, Klarna’s banking license enabled it to introduce Klarna Balance wallet (2024), savings accounts, and deposit products, allowing consumers to store money directly within the app. While these banking features do not always generate direct fees, they strengthen Klarna’s ability to earn interest income and fund lending more efficiently.

This was followed by the launch of Klarna Card debit card (2025) with built-in flexible payment options, first piloted in the US in June 2025 and then expanded further. It lets users pay directly from balance or choose Klarna payment methods per transaction.

Klarna is thereby trying to monetize the consumer journey around the purchase: discovery, intent, checkout, repayment, savings, financing, and repeat engagement. The app, search, cashback, Klarna Card, and Klarna Balance features all widen the top of the funnel, while Fair Financing and deposits deepen the financial relationship underneath it. Klarna’s 2025 acceleration in Fair Financing, alongside the 2026 addition of peer-to-peer payments in 13 European countries, further adds to Klarna’s aim to improve everyday relevance, while increasing app opens and the likelihood that Klarna becomes part of routine money movement.

The Cost Stack: How Technology and Distribution Shape Efficiency

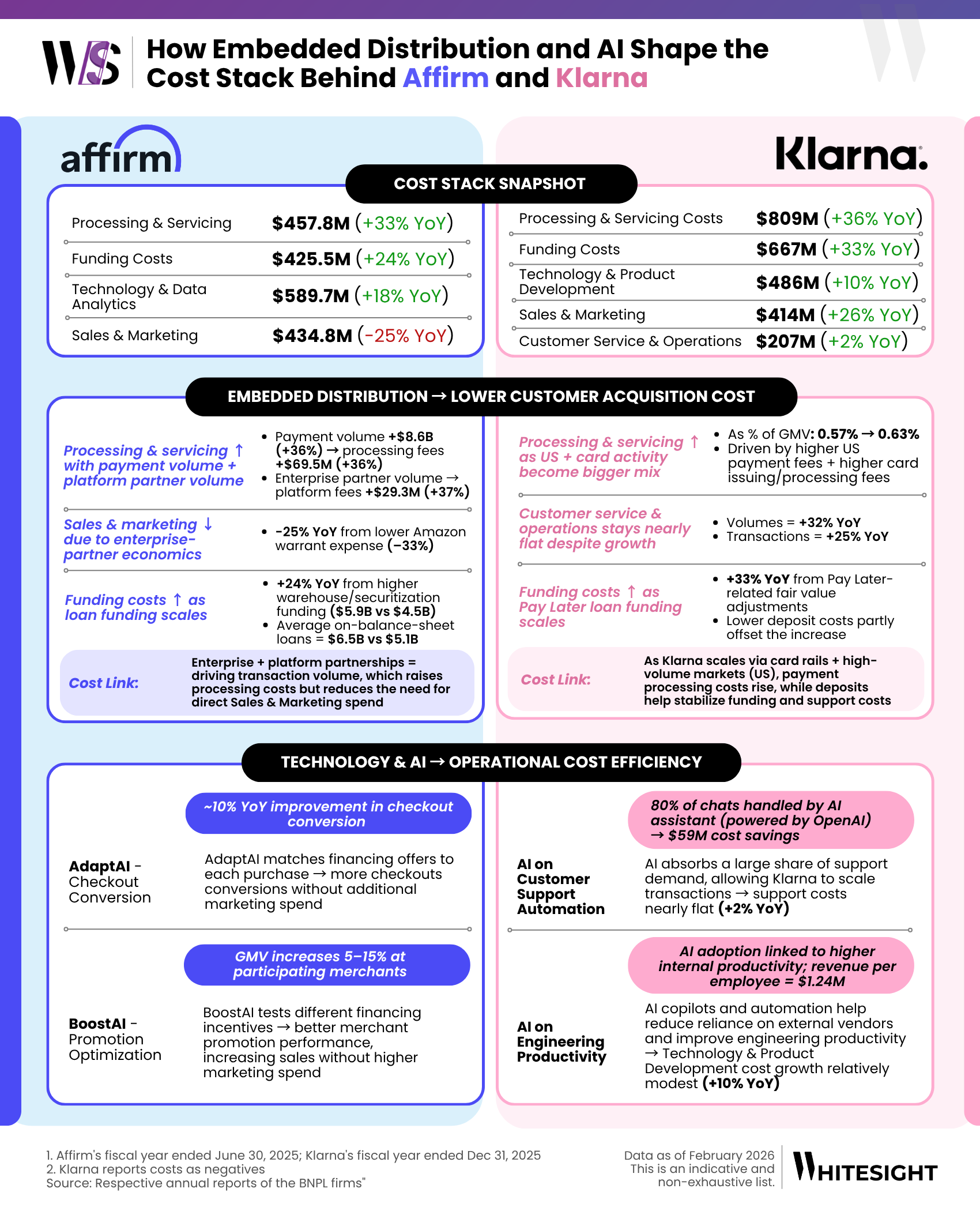

For BNPL firms, expenses generally fall into the following buckets: funding costs, processing and servicing, technology and data infrastructure, and sales and marketing. Affirm and Klarna share these same cost centers, but the way those costs scale, and the way technology and partnerships reshape them, tells a deeper story about their operating models.

Starting with funding costs, the largest structural expense for lending-driven platforms.

Affirm largely relies on capital markets funding: warehouse credit facilities and securitizations tied to its loan book. As loan volumes expand, so does the cost of maintaining that funding infrastructure. In 2025, the average funding balance tied to these facilities rose significantly (up by $1.4B, or 30% YoY) as the firm retained more loans on its balance sheet and expanded lending volumes.

Klarna’s structure looks different because of its banking license and deposit base. About 90% of its lending is funded by consumer deposits, which tend to be cheaper and more stable than wholesale funding. This gives Klarna a structural cost advantage in funding and provides a bank-like balance-sheet flexibility.

The next layer is processing and servicing, which include payment network fees, credit bureau checks, fraud screening, customer service, and collections operations. These expenses usually scale directly with transaction volume and consumer activity.

Affirm’s cost structure reflected that dynamic, with payment processing fees and servicing expenses rising in tandem with higher payment volumes and larger loan portfolios as the number of consumer transactions increased sharply in 2025.

Klarna has aggressively targeted operational efficiency in this layer through automation and AI. Its AI-powered support assistant, introduced in 2024 and powered by OpenAI, handled 80% of customer service chats by 2025, performing work equivalent to 850+ full-time agents while reducing response times and lowering support costs. Customer service and operations costs therefore grew far more slowly than transaction volumes, indicating meaningful operating leverage.

Technology spending forms the third cost layer, covering engineering talent, cloud infrastructure, data systems, and internal software. But the spending logic differs.

Affirm’s technology budget focuses heavily on risk modeling, underwriting automation, and transaction decisioning. Its systems process hundreds of data signals in seconds to evaluate fraud risk, predict repayment behavior, and price financing offers. Tools like AdaptAI improve promotional targeting and checkout conversion, which indirectly reduces sales and marketing costs by increasing the efficiency of each merchant partnership.

Klarna’s technology investment emphasizes consumer engagement and operational automation. Its AI stack powers shopping recommendations, personalized discovery feeds, underwriting models, and the customer support assistant that dramatically reduces manual service workloads. The result is a platform that can handle more activity without adding staff at the same pace.

The final layer is sales and marketing expense, which includes merchant acquisition incentives, promotional campaigns, and partner agreements.

For Affirm, embedded partnerships act like distribution assets. Its Amazon partnership (2021) expanded checkout reach at scale, but also added warrant-related costs to sales and marketing. In FY2025, sales and marketing fell largely because Amazon warrant expense declined by $135.2M (33% decrease YoY) as part of those warrants became fully vested, and because the 2024 renewal spread the partnership cost over a longer period, reducing the annual expense hit. Its Shopify partnership, which began in 2020 with exclusive US Shop Pay Installments and expanded again in 2025 into Canada and the UK, works in a similar way. Affirm accepts some upfront partnership cost in exchange for access to Shopify’s large merchant base. That makes growth cheaper over time, because Affirm can reach many merchants through one platform relationship instead of signing each one separately.

Klarna relies less on marquee partnerships and more on its app and commerce ecosystem, where merchants can reach consumers directly through discovery, advertising, and promotions.

Taken together, the cost stack reinforces the strategic divide between the two firms. Klarna uses AI primarily to compress operating costs and scale a large consumer platform efficiently, while its deposit base stabilizes funding costs. Affirm uses technology to improve transaction-level economics, pricing risk more accurately and increasing checkout conversion through smarter decisioning.

Two Futures Emerging from the Same BNPL Wave

Affirm and Klarna may have come from the same BNPL wave, but their recent moves suggest they are heading toward very different futures. Affirm is widening out into a payment network, using cards, merchant integrations, and embedded partnerships to become part of more transaction flows. Klarna is moving in the opposite direction, using BNPL as the entry point into a broader banking-like relationship built around deposits, wallets, cards, and now peer-to-peer payments.

That divergence hints at where BNPL itself may be heading. The category is beyond being the checkout feature, and evolving into either a payments layer or a financial relationship layer, depending on the strategy behind it. For merchants, this means BNPL providers are becoming more like commerce partners than payment add-ons. For consumers, it means installment credit may increasingly sit inside everyday wallets, cards, and apps rather than appearing only at checkout. And for regulators, the shift reinforces why BNPL is now being treated more explicitly as credit, bringing stronger oversight around disclosures, affordability checks, and reporting. The next phase of BNPL will likely be more about who owns the ecosystem surrounding it.

And It’s A Wrap! 👏

Hope you enjoyed this edition of Fintersections! Stay tuned for more interesting think-pieces in the coming months.

Hungry for more fintech insights? Check out some of our other work at WhiteSight.

Our latest publications include:

If you're someone who likes to stay in the know of what’s happening in FinTech, you don’t want to miss out on our bi-weekly newsletter -Future of Fintech - where we religiously track next-gen themes of the industry.

We also track Onchain Finance and Agentic AI updates.

Fintech research is in the WhiteSight DNA, so if you'd like to get in touch for features, research content, or sponsorship-related services, reach out to us at hello@whitesight.net.

And lastly, to stay updated on everything fintech, follow us on LinkedIn and Twitter and don't be shy to show some 💛

Very insightful ✨